How to Buy Property in Dubai as a Foreigner in 2026

Buying property in Dubai is easier than most first-time buyers expect — open to almost any nationality, fast on paperwork, and heavily marketed. That ease is exactly why money is rarely lost on the purchase itself.

Most of the risk sits in the decisions taken before you buy — the wrong zone, the wrong developer, a yield quoted before costs. This guide takes you through the process the way a cautious investor should: what to buy, where, and how to protect your money.

Can foreigners buy property in Dubai?

Foreigners can buy property in Dubai with full ownership, as long as the property sits in a designated freehold area and the buyer is at least 21 years old. No residency, visa or local sponsor is required — a non-resident abroad has the same right to buy as an expatriate already living in the UAE.

The legal barrier to entry is low; the risk you actually manage is what you buy and where. This right has applied to all nationalities since Law No. 7 of 2006 and is administered today by the Dubai Land Department, the government body that registers every transaction.

Where can foreigners buy property in Dubai?

Foreigners can buy in any of Dubai's 60+ designated freehold areas, which span the whole city. The simplest way to read them is in three bands — prime waterfront, established inland communities, and emerging high-growth zones to the south — each with a different price, tenant profile and yield.

Prime waterfront and central districts — Downtown Dubai, Dubai Marina, Palm Jumeirah, Business Bay and Dubai Creek Harbour — carry the highest prices and the deepest resale demand.

Established inland communities such as Dubai Hills Estate, JVC, Arabian Ranches and Dubai Silicon Oasis trade lower per square foot and suit families and yield-focused buyers.

Emerging zones to the south — Dubai South, Expo City and Academic City — offer the lowest entry prices and the highest headline yields, in exchange for a longer growth horizon.

"The zone is your first risk decision: it sets your tenant pool, your resale liquidity and your yield long before the building does. We lways confirm a property's status against the DLD's register of designated areas before committing, as new zones are added by decree over time. First-time buyers are usually best served by established communities, where resale demand is already proven and a mistaken entry is easier to exit."

Do you need residency to buy property in Dubai?

Buying property in Dubai requires neither UAE residency nor a visa, and a purchase can in fact become the route to residency rather than the reverse. Non-residents buy on the same legal footing as residents, a position confirmed in the UAE Government's official residency rules.

The only practical differences appear later, at the financing stage: banks lend a smaller share of the price to non-residents and ask for more documents. We cover those limits in the mortgage section below.

Freehold, leasehold or usufruct: which applies in Dubai?

Freehold gives you full, indefinite ownership of both the property and the land beneath it; leasehold and usufruct give you the use of a property for a fixed term without owning the land. For most foreign buyers, freehold is the relevant and preferred structure, because it carries the strongest control and the cleanest exit.

Off-plan or ready: which should a first-time buyer choose?

Off-plan means buying from the developer before or during construction; while ready means buying a completed home you can use or rent out today. The choice is the second big decision after the zone, and for a first-time buyer it carries the most risk — because off-plan now drives most of the market.

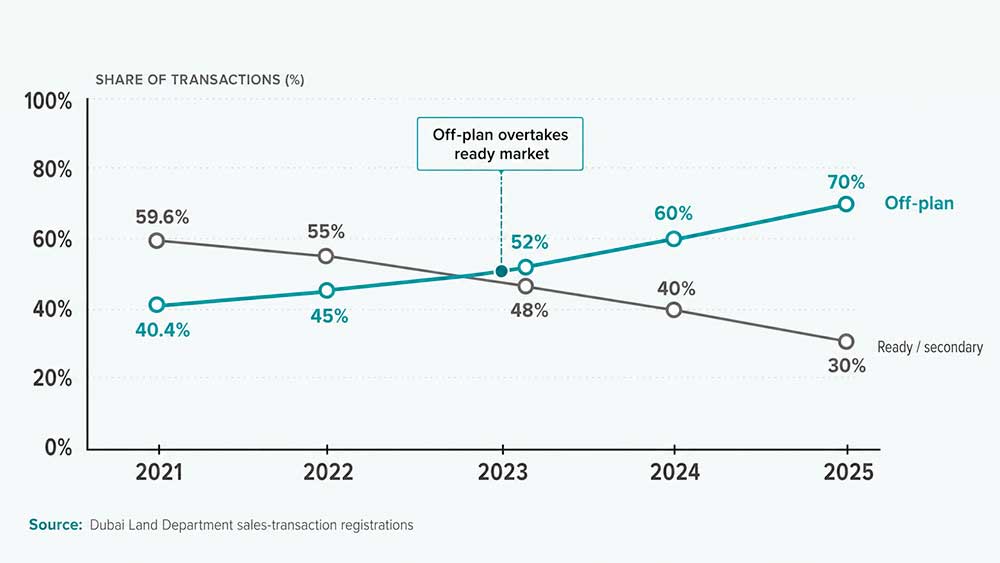

What is off-plan, and why does it dominate Dubai's market?

Sold before completion, off-plan property is paid through a staged plan across construction — and sometimes beyond handover. Its appeal is the low entry cost, the flexible instalments, and the prospect of appreciation between launch and completion, which in prime areas has averaged about 23% over the past three years, on Property Monitor's data.

The off-plan share has climbed from about 40% of sales in 2021 to roughly 70% in 2025, on Dubai Land Department data, while ready resale deals have shrunk in proportion. Buyers pay for that future: off-plan now trades at roughly a 30% premium per square foot over comparable ready stock — about AED 2,149 versus AED 1,663 — up from 17% in 2023, on Property Monitor's figures.

Off-plan vs ready: the honest trade-offs in Dubai

Off-plan and ready property answer to different buyers: one trades certainty for a lower entry and the chance of appreciation, the other pays more for income that starts now. The table below sets the trade-offs side by side.

The mortgage line alone reshapes many budgets: the UAE Central Bank caps off-plan lending at 50% of value, so an off-plan buyer needs far more cash up front than the headline payment plan suggests.

Large off-plan communities such as Dubai Creek Harbour and Azizi District are worth studying precisely because their scale shapes how much identical stock reaches the market at once.

"Most towers do get built — that's not where the risk hides. It shows up on handover day, when a hundred identical units hit the rental market at once and your first-year yield is set by your neighbours' impatience, not the brochure"

When does off-plan make sense in Dubai — and when does it not?

Off-plan makes sense when you have a long horizon, you are buying for capital growth rather than immediate income, and you have verified the developer and the escrow arrangement behind the project. Patience is the entry ticket: your money is committed long before the asset exists or earns.

Off-plan does not make sense when you need rental income now, when the larger cash requirement would stretch you, or when you are risk-averse and new to the market. We set out how to check a developer and protect your money — escrow accounts, the defect-liability period, and title verification — in the due-diligence section below.

For a first-time buyer, off-plan is justified only with a proven developer and a horizon that comfortably outlasts the construction period — otherwise ready property removes the two risks beginners underestimate, delay and handover oversupply.

How do you buy property in Dubai, step by step?

Buying property in Dubai follows a regulated sequence overseen by the Dubai Land Department, from agreeing terms to the title deed passing into your name. For a ready home the process commonly takes a few weeks; for off-plan it is tied to the construction schedule.

The sequence itself is simple. The system rarely causes delays; unprepared documents and late mortgage approvals do.

What are the steps to buy a ready property in Dubai?

Buying a ready property in Dubai runs through seven clear steps:

- Set your budget, including the fees covered in the costs section below, and — if you are financing — secure mortgage pre-approval first.

- Choose your zone and property, ideally with a RERA-licensed agent who can verify pricing and listings.

- Agree the price and terms with the seller.

- Sign the Memorandum of Understanding (Form F) on the DLD's official system and pay the standard 10% deposit, usually held by the registration trustee until transfer.

- The seller obtains a No Objection Certificate (NOC) from the developer, confirming there are no outstanding service charges on the unit.

- Complete the transfer at a DLD-approved Registration Trustee office, paying by manager's cheque along with the 4% DLD fee.

- Receive the Title Deed issued in your name.

In our experience, three things stall a Dubai transfer more than anything else:

- Unpaid service charges on the seller's side

- A seller's own mortgage that has to be cleared first

- Buyer documents or mortgage approval left until late

We confirm a unit is clear of arrears and liabilities before a client ever signs Form F.

What documents do you need to buy a property in Dubai?

You need surprisingly little to buy a ready property in Dubai:

That is the full base list for most cash purchases.

You also do not need to be in Dubai to buy. Overseas buyers can complete a purchase remotely by granting a notarised power of attorney to a representative, who signs the Form F and attends the transfer on their behalf — a route many of our non-resident clients use when flying in for a single appointment isn't practical.

How does the process differ for off-plan?

Off-plan follows a different path, because the seller is the developer itself. You sign a Sales and Purchase Agreement (SPA), which the developer registers with the Dubai Land Department through the Oqood interim-registration system. There is no Form F and no resale transfer.

Payment runs through a staged plan tied to construction, with instalments across the build. There is no seller NOC, and the Title Deed is issued only on completion and handover. Financing is tighter too: a mortgage on off-plan is capped at 50% of value, as set out in the mortgage section below.

Until handover, an off-plan buyer holds only a contractual claim; full ownership passes at completion. An Oqood registration is not a title deed. That is why, in practice, we weigh a developer's delivery record above the contract itself.

How long does buying take in Dubai?

A ready purchase commonly completes within a few weeks once documents and financing are in place — cash buyers move fastest, while a mortgage adds time for valuation and the bank's final offer. An off-plan purchase can be reserved in a day, but full ownership transfers only when the project completes, which may be years away.

The transfer itself is a single appointment at the trustee office. Preparing documents and financing early is the one lever that reliably shortens the process.

What does it really cost to buy property in Dubai?

Budget around 7–10% above the purchase price for a Dubai home. A cash purchase lands nearer 6–8%; a mortgage pushes it toward 8–10% once bank fees and insurance are counted. The headline 4% transfer fee is only the start.

The purchase is also just the first cost. A clear budget counts what you pay while you own, and what you pay when you sell.

What are the upfront fees when buying in Dubai?

The upfront fees are fixed, public and easy to total in advance:

Two points the table hides. Residential sales carry no VAT themselves — the 5% you see applies only to services like the trustee and agency fees. And on transfer day you pay by manager's cheque: one to the seller, one to the Dubai Land Department for its fee; with a mortgage, your bank issues its own cheque and settles directly.

Only one of these lines has any give. The DLD's 4% is fixed; the agency commission is the line buyers occasionally negotiate. Off-plan buyers pay the same 4% to the DLD, registered through Oqood, usually at booking.

Cash or mortgage: a worked example on an AED 2M apartment

A mortgage lowers the cash you need on day one, but it raises your total fees. Here is the same AED 2,000,000 apartment, paid two ways:

The mortgage adds about AED 24,000 in one-off costs — a Central Bank-set 0.25% registration, a bank arrangement fee of roughly 1% of the loan, and a valuation of AED 2,500–3,500. Add mandatory life insurance, paid yearly, and most mortgaged buyers land near 8% all-in. The trade is straightforward: you free up AED 1.6M of capital and pay a few thousand dirhams more in fees to do it.

What costs do first-time buyers forget?

The fee table is the easy part. The costs that catch beginners come before and after it.

Easy to miss at purchase:

- NOC fee to the developer — AED 500–5,000 (usually the seller's, but negotiable)

- DEWA utilities deposit — AED 2,000 for an apartment, refundable

- Mortgage life insurance, and any conveyancing or power-of-attorney fees

While you own: service charges are the main ongoing cost — commonly AED 10–32 per square foot a year, depending on the community. They come straight out of rental income, so we fold them into real yield in the net-yield section below.

When you sell: the costs return. Expect agency commission of around 2% again, a fresh NOC, and — if you settle a mortgage early — a fee the Central Bank caps at 1% of the outstanding balance or AED 10,000, whichever is lower. We budget the exit at the entry, because a purchase you cannot leave cheaply is not as liquid as it looks.

Can a foreigner get a mortgage in Dubai?

Yes — both residents and non-residents can take out a mortgage in Dubai. How much you can borrow turns on your residency: residents up to 80% of the price, non-residents usually 60–65%.

The borrowing limits are set by the UAE Central Bank, so they hold across every lender; what varies is the rate and how readily a bank lends to overseas buyers.

How much can you borrow as a foreigner?

Your maximum depends on residency, and on the property's value and type:

Who qualifies for a mortgage in Dubai?

Qualifying comes down to income and existing debt. Most banks look for a minimum monthly income of around AED 15,000 for salaried applicants, and more for the self-employed.

The Central Bank also caps your total monthly debt repayments at 50% of gross income — the debt-burden ratio — which includes existing car loans, credit cards and personal loans.

The paperwork is light. You will typically need:

- Passport

- Proof of income

- Six months of bank statements

- Notarised home-country documents — non-residents

A pre-approval sets your budget; the binding offer arrives only after the bank values the specific property.

What rates do mortgages carry — and how does it differ for non-residents?

As of June 2026, fixed mortgage rates for residents start at around 3.99% — among the lowest since 2021, after the Central Bank cut its base rate to 3.65% in December 2025. Indicative starting fixed rates:

Non-residents face three differences. The rate is higher — commonly 4.5–6.5%; the term is shorter — typically 15–20 years, against up to 25 for residents; and the pool of willing lenders is smaller, with only around six banks (HSBC, Emirates NBD, Mashreq, ADCB, Standard Chartered and ADIB) actively lending to overseas buyers.

In our experience, a non-resident should secure a pre-approval before property-hunting and approach more than one of those banks, because the spread between their offers is far wider than a resident ever sees.

What yield does Dubai property really pay?

Dubai's rental yields are among the highest of any major city, commonly quoted at 6.6–7% gross. The figure you actually keep is lower, once running costs come out.

Yield also varies far more by property type than any average suggests. A studio and a villa can sit nearly four points apart, so a single "Dubai yield" number tells you very little.

What's the difference between gross and net yield?

Gross yield is the simple sum: annual rent divided by the purchase price. Net yield is what remains once the running costs come out — service charges, property management, vacancy between tenants, and maintenance.

Across Dubai, net yield typically lands about 1.5 to 2 points below gross. Service charges are usually the largest deduction, billed through the DLD's service-charge index, which is why that cost shapes your real return more than any other.

How does yield differ by property type? Three scenarios

Yield falls as price and size rise. The three scenarios below — a studio, a two-bed apartment and a townhouse — show the same year producing very different returns.

What does the yield spread tell you?

A studio in JVC or Dubai Silicon Oasis can net close to double a prime villa's yield — but that higher percentage carries trade-offs. Expect more tenant turnover, a narrower pool of resale buyers, and less of the capital growth that larger homes in established areas tend to capture.

We weigh yield and capital growth together, because a high percentage on a hard-to-sell unit is rarely the win it appears to be. Emerging, high-yield communities such as Academic City sit at one end of that trade-off; prime villa districts sit at the other.

How do you check a developer and protect your money?

Dubai gives off-plan buyers real legal protection — escrow, defect warranties, a regulator that can intervene. But they shield you only if you confirm they apply before signing.

Everything else rides on the developer. The law sets the floor; the developer decides the outcome.

What protections does Dubai give off-plan buyers?

Three protections sit behind every registered off-plan project.

Escrow comes first. Under Law No. 8 of 2007, your payments sit in a project-specific account, ringfenced from the developer's creditors. The developer draws on it only against certified construction progress; if the project stalls, RERA steps in to finish it or refund buyers.

A retention buffer follows: after completion, the escrow agent holds back 5% for one year from registration, covering early defects.

Warranty cover completes the set: a one-year defect-liability period for non-structural issues (plumbing, wiring, fittings) and a ten-year structural warranty on foundations, walls and columns — set by Dubai's property law and the UAE Civil Code.

All of it applies automatically on a registered project — so confirming registration is step one.

How do you check a Dubai developer before you buy?

Checking a developer takes an afternoon and saves years of regret. Before committing, confirm:

- Delivery record — how many projects handed over, and on time?

- Project registration on the DLD and RERA, including the Oqood entry

- An active escrow account for the specific project

- Title or Oqood verification through the Dubai REST app

- Any history of long delays, disputes or RERA penalties

Across the deals we handle, a record of on-time handovers tells you more than any brochure or render.

Which developers does Mint rate high, and why?

No developer is risk-free, but track record narrows the odds. We weight delivery and backing above design and marketing:

Emaar and Meraas carry the lowest delivery risk — the state stands behind them. Emaar's Dubai Creek Harbour alone counts 10,582 completed units (see our Dubai Creek Harbour review).

Dubai Holding-backed Nakheel is the developer that quite literally redrew Dubai’s coastline — from Palm Jumeirah to Dubai Islands and the relaunched Palm Jebel Ali, where over AED 750 million in infrastructure works are scheduled for completion in Q4 2026. Imtiaz, in our experience, delivers on time in prime locations, with a strong record of price appreciation — though past performance is never a guarantee.

To compare private developers, see our Sobha, Ellington and OMNIYAT breakdown.

What are the most common mistakes first-time buyers make in Dubai?

Most money lost on Dubai property comes from a few avoidable mistakes. The ones we see most:

- Treating the asking price as the market price. Check recent DLD transaction prices before you offer.

- Budgeting only the 4% transfer fee. Set aside 7–10% for all cots (see the costs section).

- Chasing the gross yield. Work out the net, after service charges and vacancy (see net yield).

- Buying off-plan on trust. Verify the developer's record and the escrow account (see developer checks).

- Picking a zone by emotion. Match it to your goal — yield, growth or use (see where to buy).

- Buying for lifestyle, ignoring the exit. Weigh resale liquidity before you sign.

The costliest one we see is paying an asking price nobody actually transacts at — a single over-payment can quietly erase two years of yield.

None of these are sophisticated traps; they catch buyers who let excitement outpace homework. Slowing down at the right moments is most of the discipline.

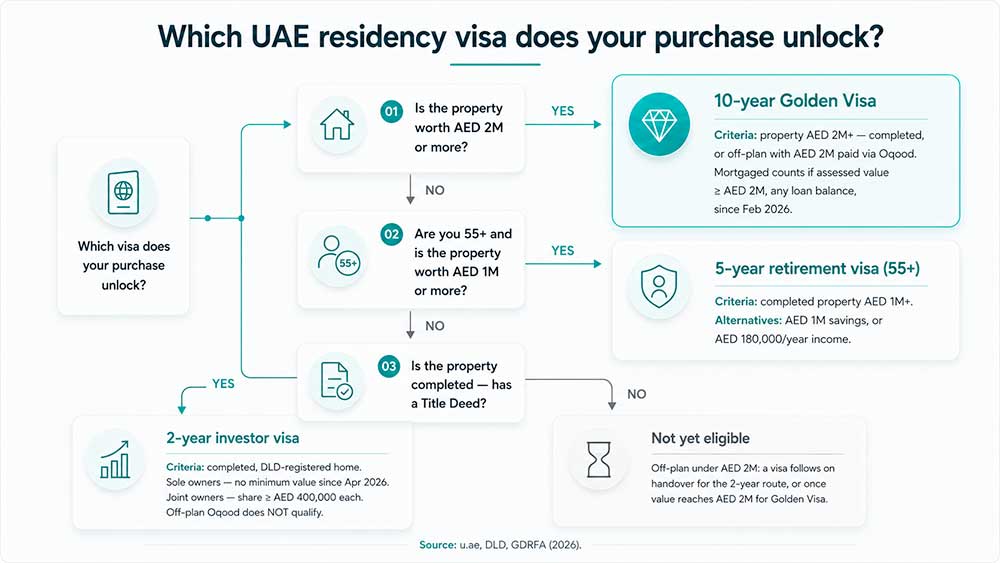

Can buying property in Dubai get you UAE residency?

Yes — and in 2026 the thresholds only got easier. A purchase can earn a two-, five- or ten-year visa, depending on its value and your age.

Which visa does your purchase unlock?

Three property routes lead to residency:

- 10-year Golden Visa — property worth AED 2M+ (completed, or off-plan with AED 2M paid). Since February 2026, a mortgaged home counts as long as its assessed value reaches AED 2M, whatever the loan balance.

- 2-year investor visa — any completed, DLD-registered home, with no minimum value for sole owners since April 2026 (joint owners need AED 400,000 each). An off-plan Oqood contract does not qualify.

- 5-year retirement visa — for buyers aged 55+, with property worth AED 1M+ (or AED 1M in savings, or AED 180,000 a year in income).

The change replaced the old AED 750,000 floor — confirmed by the GDRFA — so much of the advice still online is already out of date.

What does UAE residency actually give you?

A property visa is worth far more than the right to stay. On the family side, you can sponsor your spouse, your children of any age and your parents, and live, work or study with no employer or local sponsor — with an Emirates ID, a driving licence and access to local schools and healthcare.

The bigger draw is tax. The UAE charges no personal income tax, no capital-gains tax when you sell, and no tax on rental income for individual owners — you keep 100% of the rent — alongside no annual property tax and no inheritance tax, the one-off 4% DLD fee aside.

Hold the property through a company and its income can fall inside the 9% corporate tax; personal ownership stays outside it. You can also open UAE bank accounts and access local mortgages.

The Golden Visa adds flexibility: ten years, renewable and self-sponsored, with no six-month limit on time abroad — standard residence visas lapse after six months away, while the Golden Visa holds.

We treat the visa as a real part of a purchase's return — though the property still has to stand on its own as an investment.

Is now a good time to buy property in Dubai?

Dubai's market is cooling to a healthier pace: price growth is normalising from the 12–22% of 2024–25 toward a forecast 5–8% in 2026.

Cooling is far from weakening, though — and for most buyers the decisive question is what and where, more than when.

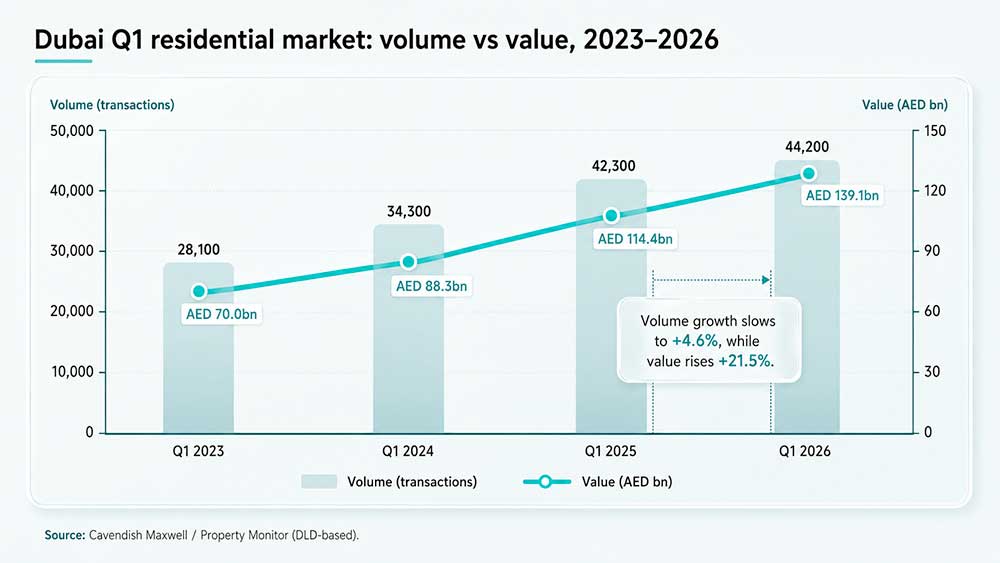

What's happening to Dubai prices in 2026?

Prices are climbing even as deal volume levels off. Sales volume rose just 4.6% year-on-year in Q1 2026 — after two years near +23% — while transaction value climbed 21.5%.

The cool-down has two drivers: fewer new launches, and a heavy pipeline of close to 300,000 units due by 2028 (Cavendish Maxwell). More supply tempers prices — hence the single-digit forecast.

Is Dubai's market a bubble, or built to last?

Dubai property has more than doubled over two decades, through the 2008 crash, oil shocks and a pandemic (DLD price index). It barely flinched at conflict, either: the Iran–Israel flare-up of June 2025 did nothing to stop Dubai's biggest year on record — around AED 917 billion across some 270,000 deals — while high-net-worth inflows rose 46%, roughly $63 billion arriving from conflict-hit countries.

"Dubai tends to strengthen when the region wobbles — instability sends capital looking for a safe home, and much of it lands here. Prices are up 60–75% since 2021, and in our experience the best entry has always been the earliest one. When the conflict fully de-escalates, the demand sitting on the sidelines comes back and prices take another leg up. Today's window will not stay open forever."

It is a forecast, and the record behind it runs to twenty years of Dubai doing exactly that. Your own return still turns on the zone, the developer and the price you pay.

Key takeaways

- The zone is your first risk decision — it fixes your tenant pool, resale liquidity and yield long before the building does.

- Off-plan is 70%+ of Dubai's market, and where beginners lose the most — verify the developer's record and the escrow account before you pay a dirham.

- Net yield is the only yield that counts — service charges, vacancy and management quietly cut the advertised gross by about a third.

- Tax and residency are the hidden returns — AED 2M earns a 10-year Golden Visa, and the UAE takes no income, capital-gains or property tax.

- Dubai didn't pause for war — it posted its biggest year on record through the 2025 conflict, and has more than doubled in two decades.

Frequently asked questions