Dubai Silicon Oasis: An Investor's Guide to the District's Second Growth Wave

Most Dubai investment stories sell a district that does not exist yet. Dubai Silicon Oasis is the opposite: an already-built, income-producing tech district now receiving a second, government-funded growth wave.

This guide gives the logic, the numbers and the trade-offs before the renders — what DSO is, what it costs, what it yields, and which new projects deserve a closer look.

What and where is Dubai Silicon Oasis?

Dubai Silicon Oasis is one of the few Dubai districts that is already finished and lived-in: a government-built, free-zone technology district in eastern Dubai, established in 2003 across 7.2 km², with around 88,000 residents and 28,000+ companies already trading. You arrive to a working community — a mall, schools, parks and office towers — not a render or a building site.

At its core are the Dubai Silicon Oasis Authority headquarters and the IT Plaza offices. Around them sit Cedre Villas (1,207 homes) and apartment communities, with everyday anchors close by: Silicon Central Mall (218 shops, a 12-screen cinema and a Lulu hypermarket), Cedre Shopping Centre, the 2.2 km loop at Lake Park, and schools such as GEMS Wellington Academy and Repton. The forward story — a AED 12.8 billion expansion and a new metro line in 2029 — is covered below.

Why Dubai Silicon Oasis's free-zone status matters to investors

Dubai Silicon Oasis is a free zone, which means it is built around employers — company headquarters and IT, semiconductor and AI firms — and the staff who rent nearby.

The tenant base is broad: 28,000+ companies across 11 industry clusters operate here. For an investor, that is the foundation of rental demand — a working tenant base, not a speculative one. The rental numbers behind it come in the next section.

Where is Dubai Silicon Oasis, and how well connected is it?

Dubai Silicon Oasis sits on Dubai's eastern side, between the E311 and Dubai–Al Ain highways and beside Academic City — central enough for the destinations that drive rental demand, if not for the beach. By car:

- Academic City — next door

- Downtown Dubai — 20 minutes

- Business Bay — 20–25 minutes

- Dubai International Airport (DXB) — 20–25 minutes

- Dubai Marina — 30–35 minutes

The Dubai Metro Blue Line opens on 9 September 2029, giving Dubai Silicon Oasis its own station on a 14-stop, 30 km line with a single-interchange link to the wider network.

For an investor, a station does three things: it widens the tenant pool to car-free commuters, supports rents, and improves resale liquidity.

It also tends to lift values. Across Dubai's Red Line, homes within a 15-minute walk of a station saw prices rise 26.7% on average — and up to 43.8% in the 10–15-minute band — according to CBRE. That is an indicator from past openings, not a guarantee for DSO.

Why invest in Dubai Silicon Oasis in 2026?

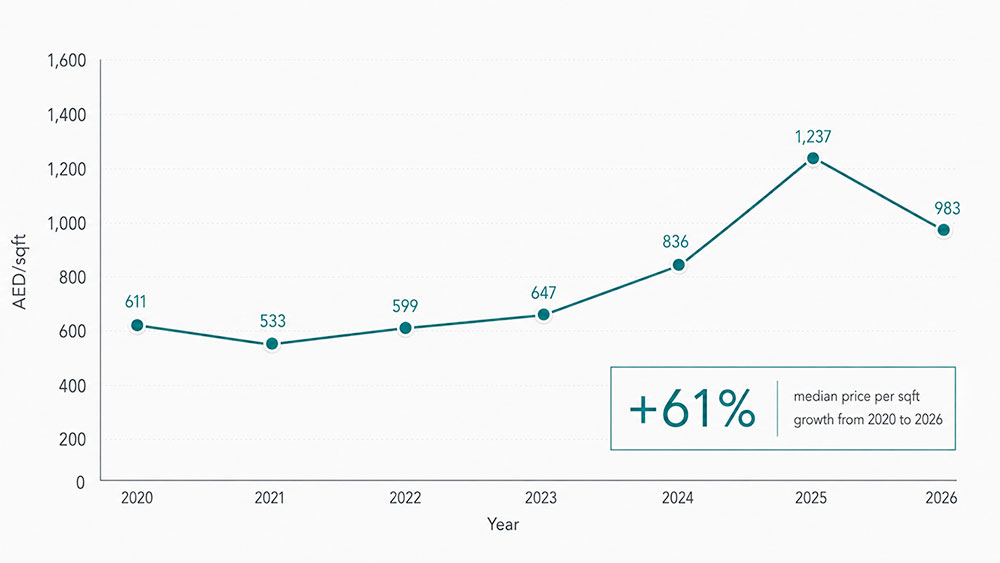

Dubai Silicon Oasis has already had its first re-rating. Median prices moved from AED 611/sq ft in 2020 to AED 983/sq ft in 2026, while the AED 12.8B expansion is only starting to be delivered and the 2029 Dubai Metro Blue Line is still ahead.

That makes Dubai Silicon Oasis investment in 2026 a timing question. The old discount has narrowed, while the next infrastructure cycle has only started. A good purchase now depends on the exact unit: price per sq ft, title, building age, service charges, achievable rent and resale depth.

Has Dubai Silicon Oasis investment already been repriced?

Yes — the first re-rating is already visible in the data. DSO is no longer priced like a forgotten outer district; the market has started to recognise its existing infrastructure, tenant base and 2029 metro upside.

The easiest return was available before that reset. In 2020–2022, investors were entering a district that looked underpriced against its fundamentals. In 2026, the question is narrower: does this specific unit still leave enough margin after the price move?

Older leasehold buildings, tired common areas and weak layouts need a clear discount. Newer projects can justify a premium when they offer better ownership, stronger rentability or a more credible resale buyer.

What does the AED 12.8B DSO expansion add?

The AED 12.8B expansion matters because it adds jobs, offices and daily infrastructure alongside new homes.

In January 2026, Dubai launched AED 12.8B of strategic expansion projects for Dubai Silicon Oasis: District IO and Block 14. District IO is planned as an AED 11B future-sector business district, while Block 14 is a residential and lifestyle district near the future Blue Line station.

For investors, the useful point is the possible increase in people who need to live near DSO rather than commute from elsewhere. That supports the rental base. A weak purchase still stays weak.

"Arabian Gate is a useful live example of how I would underwrite DSO today. Recent DLD-derived data shows studio sales in the building from AED 410K to AED 635K in April–May 2026, while comparable studio rents were recorded around AED 38K–54K/year. That spread is the real question. If the rent supports the price, the title is clean and the unit can compete, the deal may work. If not, the district story will not rescue it."

Where is the real entry price in Dubai Silicon Oasis now?

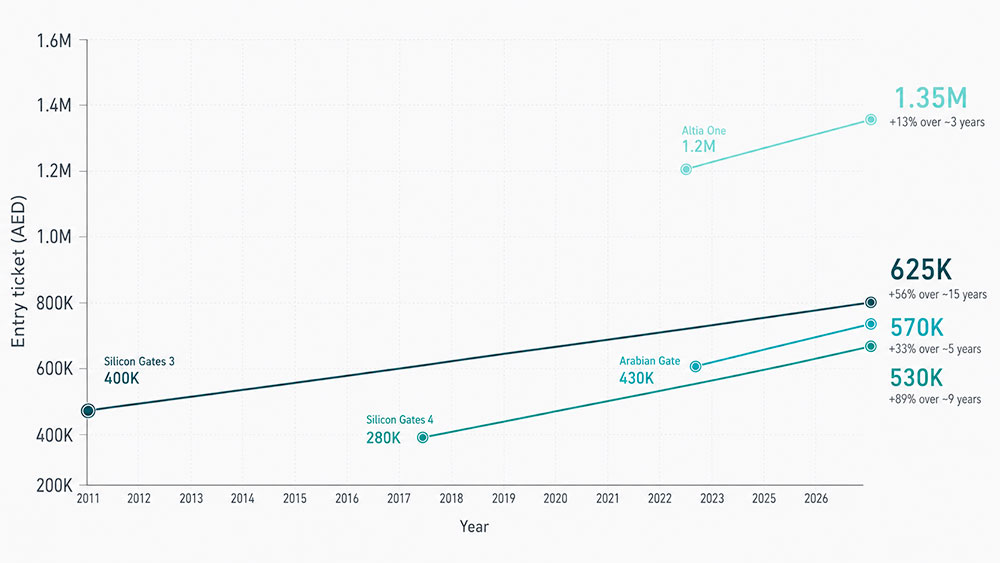

The cheapest entry still exists, but the old discount has narrowed.

The ready-project chart shows the shift across different building generations: Silicon Gates 3, Silicon Gates 4, Arabian Gate and Altia One. DSO remains cheaper than many prime and lifestyle-led districts, but the 2026 buyer is entering a different market from the 2020 buyer.

A low ticket alone cannot carry the decision. The unit has to pass three tests: today’s rent must support the price, the building must compete with nearby alternatives, and the resale buyer must have a reason to choose it later.

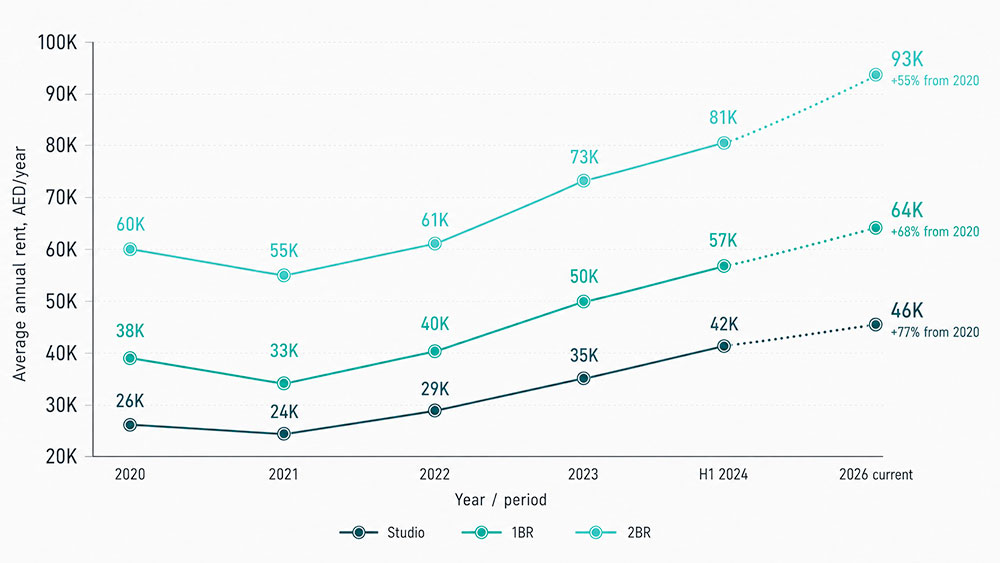

Rents have risen across studios, 1-bedroom and 2-bedroom apartments, which keeps the DSO case grounded in tenant demand rather than resale speculation.

If prices rise and rents stay flat, the investor is mostly buying a story. In DSO, the rental chart shows that tenants have absorbed higher housing costs, especially in smaller units.

What does the 2029 Dubai Metro Blue Line change?

The Blue Line should make DSO easier to rent, easier to explain and easier to resell.

Dubai Metro Blue Line is a 30 km project with 14 stations, with opening targeted for 9 September 2029. The route serves Dubai Silicon Oasis and continues to Dubai Academic City.

A station widens the audience to non-drivers, airport commuters, Academic City users and buyers who screen first by transport access. The strongest benefit should go to buildings with credible access to the station, rather than every unit using “near metro” in a brochure.

DSO is worth analysing now because the district has already moved, while part of the infrastructure story is still ahead. The right purchase is one where the numbers work before 2029. The metro should make the exit cleaner, rather than carry the whole investment case.

Is Dubai Silicon Oasis still efficient versus other Dubai districts?

Dubai Silicon Oasis is not the strongest pure yield-to-entry trade in this comparison. Dubai Sports City screens better on that narrow metric. DSO’s case is more balanced: lower entry than JVC, Arjan, JLT and Business Bay, stronger yield than most of them, an employment base, and the 2029 Blue Line.

Gross yield alone does not show the full investment picture. This table compares yield against average price per sq ft to show where investors receive more income potential per AED 1,000/sq ft of entry price.

The ranking changes the DSO story. DSO should not be bought only because the gross yield looks high. It has to win as a balanced investment: entry price, rentability, title terms, building condition, metro upside and resale depth.

"At AED 1,108 per sq ft, DSO is still materially cheaper than JVC at AED 1,455. If DSO closes even half of that gap over the next five years, the exit benchmark moves to roughly AED 1,280 per sq ft — about 16% above today’s level, before rent and costs. That is the type of scenario worth underwriting. The question is whether the specific unit can survive the downside if that re-rating takes longer."

What do yields and tenant demand say about Dubai Silicon Oasis investment?

Dubai Silicon Oasis works best where the ticket is small and the tenant pool is wide. Smaller apartments can show gross returns around 8–9%, with the final result shaped by service charges, vacancy, furnishing, maintenance and competition from similar units in the same building.

For investors, the useful question is narrow: which unit type can stay rented at the assumed price with limited discounting?

What rental yields can Dubai Silicon Oasis investment deliver?

DSO’s highest yields are usually in studios and 1-bedroom apartments.

Mint analysis based on DSO asking-rent benchmarks, asking-price samples and transaction-based pricing data. Gross yields are indicative and should be tested against live availability, service charges and recent rental evidence before purchase

Gross yield is only the first filter. A studio advertised at 9% can fall sharply after service charges, furnishing, vacancy and maintenance. The safer comparison is net yield after costs.

Who rents in Dubai Silicon Oasis?

DSO rents to practical tenants: free-zone employees, Academic City users and young families choosing the district for commute, price, space and daily infrastructure.

Dubai Silicon Oasis lists more than 28,000 companies across 11 industry clusters, giving the district a working tenant base with real employment behind rental demand.

The strongest DSO income deal is the one where rent evidence, costs, building quality and resale logic all hold together. A high advertised return matters when the unit can stay rented at the assumed rent.

Which Dubai Silicon Oasis projects are worth comparing?

Dubai Silicon Oasis has a large older-stock base, so Mint compares newer projects by one question: does the unit offer a clear advantage in price, title, layout, rentability or resale?

Availability and prices move quickly, so Mint works from live inventory, current transaction evidence and rent benchmarks.

What does Mint check before showing a DSO unit?

Mint filters out weak units before they reach the client shortlist. We shortlist the unit only when price, rent evidence, title and exit logic line up

Tria by Deyaar — lower-ticket newer stock

Tria is the accessible newer-stock route in DSO: a Deyaar residential tower with studios, 1BR, 2BR and 3BR apartments, plus larger formats such as townhouses, duplexes and penthouses.

Tria’s advantage is access. It gives investors a way into newer DSO inventory without starting at the highest-ticket end of the market. The broad unit mix also helps liquidity: smaller units suit income buyers, while larger layouts can attract families and end-users.

The Hillgate by Ellington — design-led premium

The Hillgate is the higher-ticket design-led route in DSO: an Ellington project with studios, 1BR, 2BR, 3BR and 4BR apartments, with handover targeted for Q4 2027.

The Hillgate’s advantage is identity. In a district with many older buildings, an Ellington project gives the unit a clearer reason to stand out for tenants and future buyers.

The timing is also useful. Q4 2027 handover gives the project a window before the 2029 Blue Line opening, which can support the resale case if the entry price stays disciplined.

We have also collected the most liquid new-build and ready projects in DSO into one catalogue — including Tria, The Hillgate, Altia One and Arabian Gate. Use it to compare entry price, payment plan, yield logic, title terms and best-fit buyer before choosing a unit.

What can go wrong with Dubai Silicon Oasis yields?

Dubai Silicon Oasis can show attractive gross yields, but the trap is confusing headline yield with net return.

1. The first risk is net-yield erosion: unavoidable costs can turn a strong-looking gross return into a much thinner real return. A studio bought for AED 600,000 with AED 56,400 annual rent shows 9.4% gross yield. After AED 12,000 service charges, AED 2,000 maintenance and one vacant month, net income falls to roughly AED 38,700 — about 6.4% net. The deal may still work, but the risk profile has changed.

2. The second risk is using asking rents as proof. If a unit is listed at AED 60,000/year but similar signed rents sit closer to AED 54,000, yield on a AED 650,000 purchase drops from 9.2% to 8.3% before costs.

3. The third risk is resale. Older leasehold stock, tired common areas, weak layouts and buildings with many similar units need a discount. A 2029 metro station can improve the district’s liquidity, but it will not fix a poor floor plan, high service charges or title terms that reduce the resale pool.

Top 5 investor takeaways

- DSO has already had its first re-rating.

Prices moved from AED 611/sq ft in 2020 to AED 983/sq ft in 2026, after a AED 1,237/sq ft peak in 2025. The easy discount has narrowed; the investor now needs a unit-specific margin. - DSO still offers a strong yield-to-entry balance.

At 7.91% gross yield and AED 1,108/sq ft, DSO is cheaper than JVC, Arjan, JLT and Business Bay, with stronger yield than most of them. Dubai Sports City screens better on pure yield-to-entry. - The AED 12.8B expansion supports demand, not weak unit selection.

District IO and Block 14 are planned to add 6,500 companies, around 70,000 jobs and up to AED 103B in GDP impact by 2036. That strengthens the rental catchment, but it does not rescue poor layouts, high charges or weak title terms. - The 2029 Blue Line should improve exit quality.

The Blue Line is planned as a 30 km, 14-station extension, with opening targeted for 9 September 2029. For DSO, it can widen the renter and buyer pool. The unit still has to work before the station opens. - Headline yield is the easiest trap.

A studio showing 9.4% gross yield can fall to roughly 6.4% net after service charges, maintenance and one vacant month. Treat yield as a starting point, not a verdict.

FAQ